Private label has crossed a threshold the industry is still catching up to. It is no longer the cheap option at the bottom of the shelf. It is becoming the preferred choice – generating USD 282.8 billion in US retail sales in 2025, growing at triple the rate of national brands, reaching 99% of American households, and producing a USD 90 billion franchise that rivals the revenue of the world’s largest consumer goods companies. The power in consumer goods is shifting – quietly, structurally, and faster than most brand managers are willing to admit.

Private label has reached a turning point – and it is not a cyclical one

For decades, the conventional wisdom held that private label was a defensive play. Retailers stocked it as a price anchor. Consumers bought it when budgets tightened. National brands tolerated it as background noise. That dynamic was comfortable for everyone – including, in its own way, the brands being challenged.

That comfort has become a liability. In 2025, private label products in the United States generated USD 282.8 billion in retail sales – a record high according to the Private Label Manufacturers Association and Circana1. As recently as April 2026, Walmart announced a redesign of its Great Value brand in direct response to accelerating consumer adoption of store brands – the clearest signal yet that private label investment is now a continuous strategic commitment, not a one-time launch decision. The category has grown 30% since 2021, adding nearly USD 65 billion in new revenue, while national brand unit volumes have declined by close to 7% over the same period2. Private label has now outpaced national brands in both dollar and unit sales growth for three consecutive years. This is not a recession story. Consumers are not settling. They are choosing. Premium store brands now account for 40% of private-label spend, according to Numerator – a signal that the quality ceiling consumers once assigned to own-label products have largely collapsed.

McKinsey named this a structural turning point in November 2024 – private brands shifting from opportunistic volume plays to genuine strategic alternatives that consumers actively seek out, not merely accept. The distinction matters. A consumer who switches to private label out of necessity tends to switch back when economic pressure eases. A consumer who switches because the product is good – or better – does not. That is not the language of compromise. McKinsey finds that more than 80% of US consumers now rate private-brand food quality equal to or better than national brands3, and nearly 90% say private brands offer similar or better value. That is the language of preference.

The Numerator data is the most arresting signal of all. 27% of consumers, in a recent study, did not know they had purchased a private label product4. A quarter of category buyers cannot distinguish at the moment of consumption between a national brand and a retailer’s own label. When a consumer cannot tell the difference, the brand premium – the entire financial rationale for paying more – begins to dissolve.

USD 90 billion in a red vest: what Kirkland Signature proves

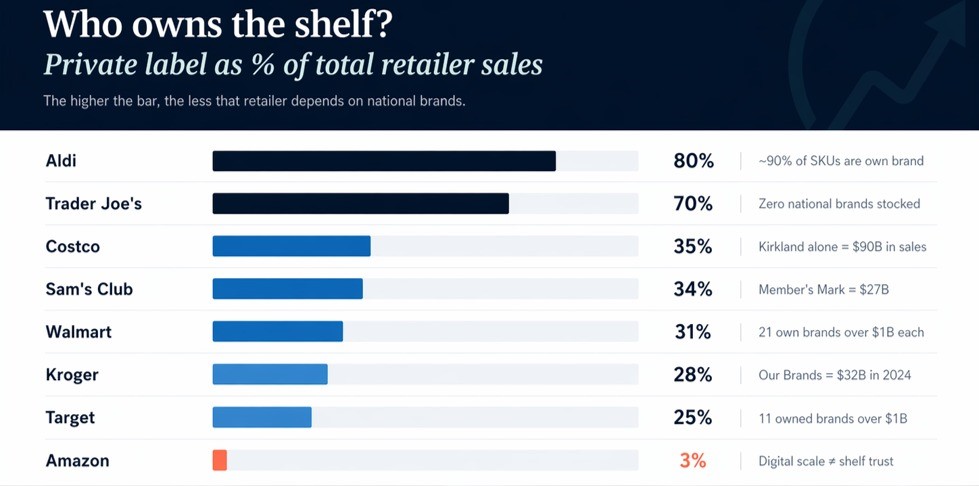

Costco’s Kirkland Signature is not merely a successful store brand. It is the clearest proof-of-concept the industry has produced for what private label becomes when a retailer commits to it fully.

Kirkland generated approximately USD 90 billion in annual sales in 2024, according to Fortune5. That figure would place it, as a standalone company, among the largest consumer goods businesses in the world – ahead of Colgate-Palmolive, roughly equivalent to Mondelez International. A private label that started as a warehouse club offering on commodity items has become, by revenue, one of the dominant consumer goods franchises in existence.

What Kirkland demonstrates is that private label’s ceiling is set by the retailer, not the category. Kirkland products are frequently co-manufactured by the same suppliers who produce the category’s leading national brand, often to tighter quality specifications. Consumers trust Kirkland not because Costco has convinced them to lower their standards – but because Costco has raised Kirkland’s standards to match or exceed what they expected from established brands. The store brand is a manifestation of the retailer’s promise, and that promise, maintained consistently across thousands of SKUs over decades, has built institutional brand trust that most national brands spend hundreds of millions in advertising annually trying to replicate.

The Kirkland lesson is not that every retailer can replicate Costco’s model. It is that the ceiling for private label quality and consumer trust is far higher than the industry’s historical framing suggested – and that the retailers who invest in closing the gap between store brand and national brand experience are capturing not just volume but loyalty that does not reverse.

Who is winning – and what their numbers say

The private label transformation is not being driven by a single retailer or a single strategy, offering important. It is being executed across the competitive spectrum – from warehouse clubs to discount grocers to mass merchants to pharmacy chains – with meaningfully different approaches but a shared underlying logic: own the product, own the margin, own the customer relationship.

Take the major retailers. While their approach to private label has differed, they have scaled the business to occupy what was essentially the shelf space for national brands.

| Retailer | Brand(s) | Positioning & strategy | Key result | What it signals |

| Costco | · Kirkland Signature | · Single umbrella brand across all categories· Premium quality parity· Co-manufactured with national brand suppliers to tight specs | · ~USD 90 bn in annual sales (2024)· 35% of total Costco revenue· 43% US household penetration | · Proves private label can carry premium positioning and become a standalone brand identity at global scale |

| Walmart | · Great Value· Equate· Bettergoods· Marketside | · Multi-tier portfolio from everyday value to elevated food· Bettergoods launched May 2024 – first major new brand in 20 years· 300 SKUs across frozen, dairy, snacks, beverages | · Walmart US now has 21 private brands each exceeding USD 1 bn in annual sales,6 including 5 exceeding USD 5 bn (Walmart corporate, April 2025) | · Scale-backed multi-tier strategy captures every consumer value segment simultaneously; Bettergoods signals competing on quality, not just price |

| Target | · Good & Gather· Up & Up· Dealworthy· Favorite Day | · Design-led, lifestyle-positioned own brands· Dealworthy launched Feb 2024 for price-sensitive basics (400 items, most under USD 10, some electronics 50% below any other Target brand)· Good & Gather as premium food identity | · Own and exclusive brands account for approximately one-third of total Target merchandise sales· 11 owned brands individually exceed USd 1 bn in annual sales7 (Target 2024 Annual Report) | · Design investment signals premium aesthetics are now table stakes in private label – not a differentiator |

| Aldi | · Aldi (full own-brand model) | · Near-total private label (~90% of SKUs)· Advertising-free cost structure passes savings to shelf price· Full brand refresh announced 2025 | · 80% of units sold are own brand· Store visits up 7.1% in 2025· Fastest-expanding major US grocery format8 | · Entire business model predicated on private label – proves the model is structurally viable at scale without a single national brand |

| Trader Joe’s | · Trader Joe’s (full own-brand model) | · Premium private label with cult positioning· Seasonal and innovative SKUs; high design investment· Accessible price points | · ~70% of total sales from own brand; store visits up 11.9% in 2025· Among highest consumer loyalty scores of any US grocer | · Demonstrates private label can carry full brand equity and cultural cachet without stocking a single national brand |

| Kroger | · Private Selection· Simple Truth· Smart Way· Field & Vine | · Tiered portfolio covering premium, natural/organic, and everyday value· Smart Way launched fall 2022 as value-focused grocery line· Field & Vine launched 2024 as a produce brand | · Our Brands portfolio generated over USD 32 bn sales in 20249· Smart Way +135% YoY in H1 2024 (Kroger 2025 Responsible Business Report) | · Tiered architecture allows simultaneous competition at premium, mid, and value tiers – reducing national brand leverage at every category level |

| Sam’s Club | · Member’s Mark | · Warehouse club model; premium quality framing analogous to Kirkland· Cross-category coverage across food, apparel, and home | · USD27 B+ in annual Member’s Mark sales; 34% of total Sam’s Club revenue | · Second proof point after Kirkland that warehouse retail is uniquely suited to building high-trust private label at scale |

| CVS Health | · CVS (own brand), Well Market | · Pharmacy-adjacent health, beauty and wellness· Well Market launched 2024 as a premium wellness line extending the pharmacy trust halo into adjacent categories | · CVS brand reaches 40% US household penetration· Well Market among fastest-growing new private labels in 2024-25 | · Shows pharmacy trust halo extends powerfully into beauty and wellness – a category national brands assumed was theirs |

| Amazon | · Amazon Basics· Amazon Essentials· Amazon Saver· Amazon Grocery | · Digital-native private label; Amazon Saver launched 2024 as discount grocery; Amazon Grocery launched Oct 2025 | · Only 3% of Amazon’s total sales volume from private label – lowest of any major US retailer; Amazon Grocery gaining traction post-launch in early 2026 | · Digital shelf advantage alone does not generate the retailer-consumer trust that makes private label work. Physical retail experience still drives adoption |

| Ahold Delhaize | · Own-brand portfolios across US and European banners (Food Lion, Stop & Shop, Albert Heijn) | · Aggressive own-brand expansion across value, health, and premium tiers simultaneously· 2025 rollout prioritised healthier formulations and entry-price products across US and European markets | · 1,100 new own-brand products launched in US banners and 1,450 in European banners in 2025 alone10· Management flagged further own-brand growth as a strategic priority (Ahold Delhaize Annual Report 2025) | · Shows private label expansion is now a coordinated global portfolio strategy, not a market-by-market reaction – volume of own-brand innovation is itself becoming a competitive signal |

The margin arithmetic explains why every major retailer is doubling down. Private label margins for grocery retailers typically exceed 40%, compared to 25–35% for national brands sold through the same shelves. Every unit of own-label product sold is simultaneously a revenue event, a margin improvement, and a customer data capture. The economics compound in the retailer’s favour in ways that individual category analyses consistently understate.

The Amazon row is worth pausing on. At just 3% of sales volume, Amazon’s private label underperforms every major physical retailer by a wide margin. The implication is structurally important: digital convenience alone does not generate the trust that makes private label adoption work. That trust is built through physical experience, product encounter, and the accumulated credibility of a retailer that has consistently delivered on its implicit quality promise. Amazon has the logistics infrastructure. It does not yet have the trust architecture.

The grocery battlefield: where private label is redrawing the map

Grocery is the only major product sector with 100% private label household penetration in the United States – a statistical floor through which private label has long since broken. Private label grocery unit share reached 23.8% in the first half of 2024, up half a percentage point year on year.11 Refrigerated categories posted 7.5% dollar growth – among the highest of any grocery segment. General merchandise categories – office, home and garden, tools – have ceded between 27% and 37.8% of category unit sales to private label. These are not the movements of a category in retreat; they are the movements of a category consolidating a structural position.

European grocery markets have been living this reality for longer, and the European trajectory offers a forward indicator for the US. Private label accounted for 39% of Europe’s grocery market value in 2024 – approximately USD 412 billion in sales – with Spain, Switzerland, and the United Kingdom leading adoption.12 Switzerland has reached 52.3% private label share, and the combined share across Germany, the UK, and France sits at 40.3%, according to PLMA International. UK retailers like Marks & Spencer and Tesco have built own-label ranges that are, in some categories, the aspirational choice rather than the fallback. US grocery is at an earlier stage of this journey, but the destination is now visible.

The structural advantage retailers hold is control over what the consumer sees first. Shelf placement, promotional priority, digital positioning in click-and-collect and delivery platforms – all instruments that retailers deploy in favour of their own labels without needing to outspend national brands above the line. Every category review that grants own-label products premium shelf position is a compounding investment in private label visibility that does not appear on any national brand’s competitive radar as a conventional threat.

Beauty and personal care: the category no one expected private label to win

Beauty was supposed to be national brand territory in perpetuity. Purchases driven by aspiration, identity, and emotional association – these were assets that commodity private label could never replicate. That logic was right about commodity private label. It was wrong about what private label was becoming.

Health and beauty private label already reaches 99.2% of US households, with a unit share of 17% and a consumer trust score of 68% – the highest of any major product sector. The white label and private label cosmetics market is one of the fastest-growing segments in beauty, as retailers across mass, mid-market, and prestige tiers develop own-label ranges with production quality and aesthetic ambition previously reserved for heritage brands.13 Grand View Research projects sustained compound annual growth through the end of the decade.

The mechanism is different from grocery, and the difference matters. In beauty, the disruption has been accelerated by the decoupling of brand discovery from traditional advertising. Social commerce and influencer-driven discovery have disrupted the scale advantage of national brands in ways the industry is still calibrating. When a product goes viral because of its efficacy – demonstrated visibly in real time by a creator with audience trust – the brand identity of the manufacturer matters less than the product’s performance.

Dupes have become mainstream behaviour, not niche behaviour. Consumers openly research and share private label alternatives that deliver comparable results at lower price points – and the cultural status once attached to owning the national brand original has shifted, in some demographics, toward the savvy discovery of the effective alternative. The question brand managers in beauty must now answer honestly is: what proportion of the premium we charge covers genuine product superiority – and what proportion covers marketing infrastructure that the consumer is no longer valuing?

What the power shift actually means

The redistribution of value in consumer goods – from national brand manufacturers toward retailers – is a slow-moving but increasingly irreversible dynamic. Private label is both the symptom and the instrument of that redistribution.

Historically, national brands wielded power in the retailer relationship because their consumer pull was non-negotiable. A retailer that didn’t stock Heinz, P&G’s portfolio, or Coca-Cola’s range risked losing consumers to competitors who did. That pull created leverage in trade negotiations, shelf placement discussions, and promotional co-investment conversations. The leverage was real because the brands were genuinely indispensable.

Private label growth erodes that indispensability category by category. When a retailer’s own-label ketchup commands 30% category share, Heinz’s negotiating position at that retailer is measurably weaker than when own-label share was 10%. And every consumer who switches from a national brand to own label within a retailer’s environment is a consumer whose loyalty to that category is now expressed through the retailer’s brand, not the manufacturer’s. The retailer has captured the relationship.

The EY India research found that 52% of consumers have switched or intend to switch to private label providing valuable – and even accounting for India-specific market context, the directional signal is global.14 Consumers in categories where quality parity is achievable are treating private label as the rational default. Once a consumer makes that call and is satisfied with the product, they do not tend to return to the premium tier without a compelling reason.

Kearney’s 2024 Private Label Report projects that private label will capture an additional 7% of US dollar market share from national brands by 2030, pushing total own-brand share to 24% across the retail landscape.15 The brands that treat that projection as an overstatement are making the same error they made a decade ago, when private label’s rise from 15% to 20% share seemed gradual enough to manage comfortably.

Where national brands must respond – and where they cannot

Understanding private label’s structural rise does not require concluding that national brands are finished. It requires a clear-eyed assessment of where brand premium remains defensible and where it does not.

The categories where national brand equity is most durable share recognisable characteristics. They tend to involve genuine formulation differentiation difficult to replicate at contract manufacturer scale.16 They tend to involve emotional associations – with occasion, identity, or heritage – that are not purely functional. Luxury spirits, premium confectionery, and personal care categories with genuinely proprietary active ingredients are examples where brand premium has historically proven resilient.

The categories where national brand premium is most exposed are those where functional performance is the primary purchase driver, quality parity is achievable at private label price points, and consumer habit has been disrupted enough by inflation or product trial that brand habit is no longer protecting share.17 Much of ambient grocery, a significant portion of household care, and the rapidly growing value tier of beauty fall into this exposed territory.

The most strategic response available is clarity of focus – a ruthless prioritisation of categories and markets where brand premium remains defensible, combined with a willingness to exit or deprioritise categories where private label parity has been achieved. That clarity requires institutional honesty that large organisations with legacy category commitments find genuinely difficult to exercise. But the brands that execute it will preserve margin and relevance. The brands that do not are financing a defensive war in categories they are gradually losing, with resources that could be deployed in categories they could still win.

Where private label still fails

Private label is not invincible. The model underperforms when:

· quality is inconsistent across the range

· when innovation is thin relative to the national brand

· when the retailer overextends into categories where specialist manufacturer trust remains concentrated and difficult to replicate – In fragrance, prestige skincare, and premium spirits, brand provenance is part of the product – and own-label alternatives consistently fail to close the trust gap

The more common failure mode, though, is strategic rather than operational: treating private label as a price-only instrument. The retailers consistently outperforming on private label – Costco, Trader Joe’s, Target – all treat it as a brand architecture decision, not a discount mechanism.18 The ones that do not invest in packaging, product development, and category positioning find that private label stabilises volume but does not build the loyalty or margin premium the model is capable of generating.

The retailer is now the brand. The brand is now the challenger.

The strategic shift that private label represents is ultimately a shift in the unit of competitive analysis. For most of the twentieth century, the dominant frame in consumer goods was the brand as the primary value-creating entity. Brands aggregated consumer trust, commanded shelf space, and drove category economics. Retailers were, in this frame, important but ultimately subordinate distribution partners.

That frame is inverting. The retailer who has invested seriously in private label capability is now a brand owner, a manufacturer in all but name, and a direct competitor to the national brand portfolio it simultaneously stocks. The conflict of interest is structural and explicit – and the retailers winning in this environment are those who have leaned into it, not managed it as an awkward tension.

The consumer goods companies that will perform best through this transition are those that understand the new competitive frame clearly. They are no longer competing primarily against other national brands for consumer preference. They are competing against the retailer itself, in the retailer’s own store, with the retailer setting the terms. That is a fundamentally different strategic challenge – and it requires a fundamentally different response, built on genuine differentiation, innovation intensity, and a willingness to accept that the era of brand premium sustained by advertising alone has passed.

Private label is not the cheap option. It is the option that an increasing number of consumers are choosing actively, repeatedly, and without apology. The question for national brands is not whether that choice is legitimate – the market has answered that question conclusively. The question is what they are going to do about it.

Eliminate guesswork. Embed insight. Indigrowth.

3. McKinsey & Company. Private Brands: The Turning Point. November 2024.

6. Fortune. Kirkland Signature, Costco’s Private Label, Hits $90 Billion in Annual Sales. 2024.

16. Kroger Co. 2025 Responsible Business Report. [Our Brands >$32 billion in sales in 2024].

17. Ahold Delhaize. Annual Report 2025. [1,100 new own-brand products in US; 1,450 in Europe].

18. Reuters. Walmart Redesigns Its Great Value Private Label Brand. April 2026.